All About Your Credit Score

What is a credit score? Why does it matter? If you’ve ever asked these questions, this post is for you! We are here to explain exactly what your credit score is and why it matters — especially when it comes to purchasing a home.

Before we dive in, remember this: no matter what your credit score is today, it can be improved. If you’ve made mistakes with your finances in the past, keep your chin up. With the right knowledge and diligent effort, you can improve your credit standing faster than you might think!

What Is A Credit Score?

Your credit score is a number between 300 and 850 that represents your credit standing. A higher one indicates financial trustworthiness, while a lower one represents a poor history of paying bills and debts. Lenders use credit scores to determine a customer’s creditworthiness. Anytime you attempt to borrow money, your score is pulled by the financial institution so they can determine your buying power. The better your score, the better your loan terms.

So, what exactly affects your credit score? Let’s take a look at the factors at play.

What Impacts It?

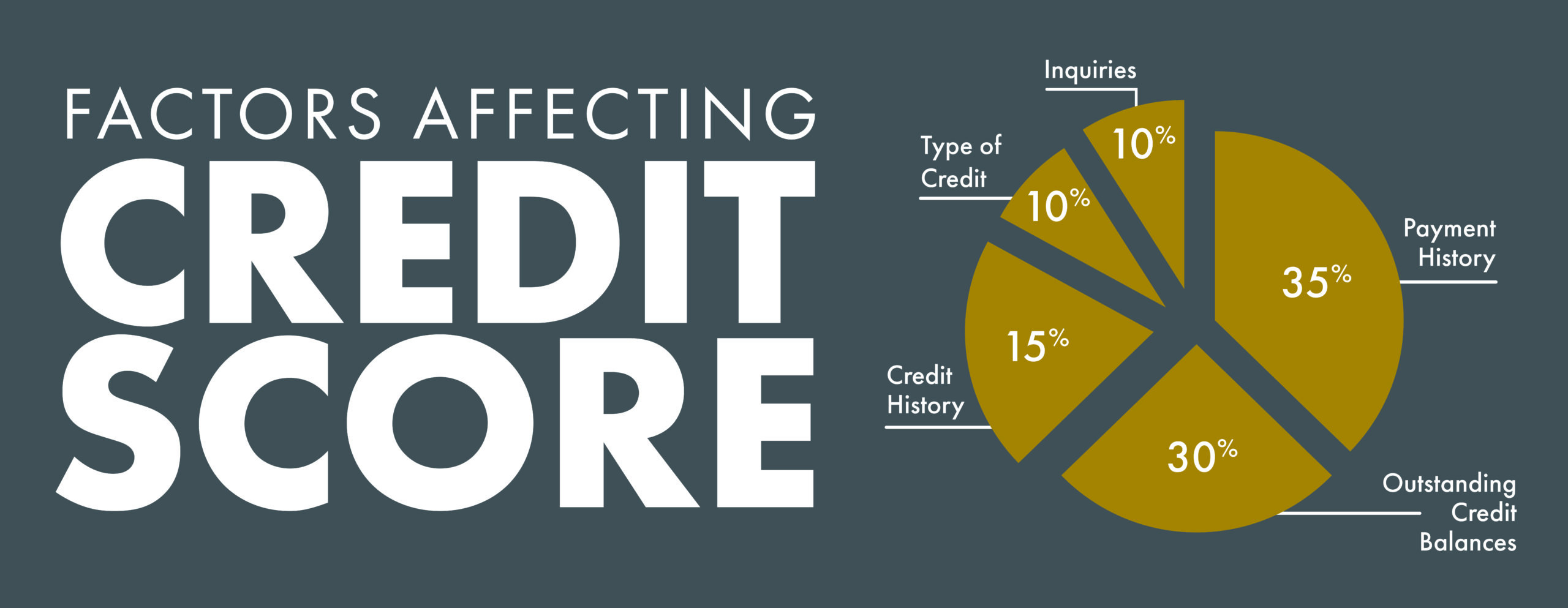

Most people think that credit scores are determined by paying bills on time. While this is a factor, it’s not the only one. The factors impacting your credit score are more sophisticated than you might think. Here are all the pieces that make up the credit score pie:

1.Your payment history includes things like paying bills on time and not having any payments that are over 30 days late (😬). Also, having a late payment of a high amount will be more detrimental than having a late payment of a lower amount. Any delinquent payments on your history that have occurred within the past 2 years will lower your score, while anything older than 2 years will not be as unfavorable.

2.Your outstanding credit balance to available credit ratio is the next largest factor in your score. In other words, have you racked up a credit card to the maximum amount? That is going to affect your score. The lower your outstanding balance and the higher your available credit, the better that is going to look to a potential lender.

3.Credit history is also a factor in your overall score. The longer you have a line of credit, the better your score. Having a long-standing line of credit indicates that you have a strong history of borrowing and paying.

4.💡Believe it or not, the type of credit you have also plays a role in your score. Having a mix of different types of credit like auto loans and mortgages (not just credit cards) will look better on your credit report and help boost your score.

5.Another factor many people don’t consider is credit inquiries. When your credit is pulled multiple times in a 6-month period, it does not look good for you as a borrower and will impact your credit score. Note that there is a difference between a hard inquiry and a soft inquiry. Hard inquiries occur when a financial institution pulls credit to open a new line of credit for you. A soft inquiry is when you or another entity looks at your credit to simply check or prequalify. Soft inquiries do not affect your score.

Check out this infographic to learn the truth about common myths surrounding credit scores!

How to Improve Your Credit Score

Now that we’ve covered all the factors that can affect your credit score, the way to improve your credit score is much more clear! Here are the top ways you can begin to improve your credit standing.

- Make payments on time! Auto-payments are your new BFF. Any time you can, set-up payments to auto-draft on the due date from your bank account to ensure you never miss a payment.

- Check your mail. We know, we know… it sounds so simple! But seriously. If you have any outstanding payments or issues with financial institutions, you’re going to get mail about it. In our digital world, it can be tempting to trash snail mail, but be sure you check and read mail from entities you’re financially involved with.

- Keep your credit balances low! The rule of thumb is to keep your credit balance 30% or below the credit limit.

- Keep your credit lines open! Do not close accounts just because they are paid off. The longer your accounts are open, the more credibility you have.

- Maintain various types of credit — not just credit cards. But before opening up a new line of credit, it is best to speak with a financial advisor.

- Don’t allow your credit to be pulled often. Companies must have your written consent to pull your credit, so anytime you’re being asked to sign something for a credit pull, it’s going to affect your credit score.

We are confident that if you follow these tips, you can improve your credit score! We are always available to help if you want to discuss your credit standing and prepare for your home purchase.

We hope this has answered all your questions about credit scores and how to improve yours. If you’re thinking about purchasing a home in the next few years, NOW is the time to start thinking about your credit! Meet with one of our Loan Officers to get the ball rolling and ensure the BEST loan rate possible for you and your family.